The Consumption Tax – A Non-Starter

By Duncan Whitmore

In a recent essay published on this blog1, the present author proposed a short series of aims that would reduce the burden of taxation on economic prosperity, in comparison to a programme proposed by the Adam Smith Institute (ASI).2 Part of the ASI’s programme consists of “replacing [the] income tax with a progressive consumption tax, so savings are not taxed”.3 In relation to this, we explained, briefly, that all taxes are paid for out of one of two sources of production – either income or wealth – and that

The individual names of all of the different taxes refer not to fundamentally different types of tax; rather, they denote either the specific kind of good to be burdened (i.e. property, alcoholic beverages, etc.) or the particular event that triggers the tax liability. For example, within the category of taxes on income, an income/payroll tax taxes the income at the point it is earned; a VAT or sales tax, on the other hand, taxes the income at the point it is spent.

Consequently, we concluded that a proposal for a consumption tax amounted to little more than simply moving a tax burden around and calling it a different name rather than eliminating its depressing effects upon economic prosperity:

Changing the precise moment when a tax is levied ultimately does nothing to ameliorate the effects of the tax – it simply means that you might be able to hang on to your money for a little bit longer before having to give it up. Neither also does changing the triggering event have any effect upon who, ultimately, pays for the tax. All taxes must be paid for out of production and so the burden of any tax always falls upon producers.

This essay will elaborate on why, for a programme that wishes to give a serious boost to economic prosperity by reforming taxes, the proposal to switch to a consumption tax from an income tax is a relatively pointless endeavour which should not be considered as a priority. We will also explain why the claim that “savings are not taxed” is utterly fallacious before exploring some particular difficulties that are inherent to introducing and operating a consumption tax. Although this essay concerns, mainly, the effects of a consumption tax upon economic prosperity, we will then move on to highlighting some further problems this method of taxation presents from a purely libertarian perspective. Finally, we will conclude by pointing out that any benefits a consumption tax could bring are unlikely to be realised in the absence of fostering a general government commitment to lower tax rates.

The Supposed Benefits of a Consumption Tax

In order understand the full logic of typical arguments in favour of a consumption tax, one has to trace through their steps very carefully.4

First, when people go to work, a tax on their earnings will leave them with fewer funds to either consume on the one hand or to save/invest on the other, and the overall incentive to work towards either will be diminished. Consequently, production all round will be lower. Step (A), therefore, seeks to remove this disincentive by taxing consumption rather than earnings.

Second, if a person’s earnings are taxed at source then there is no incentive to save this money ahead of consuming it – his money is taxed regardless of how he wishes to spend it. Therefore, step (B) proposes to tax the portion of his income that is consumed but to not tax the portion of his income that is saved so that he has a greater incentive to avoid consumption and channel his money into saving.5

Third, if there is a tax on the return from savings/investments (i.e. on the interest/dividends that the investment attracts) but there is no tax on consumption then the incentive towards saving/investment is penalised whereas consumption is not. Therefore, there will be more consumption and less saving/investment. Thus step (C) proposes to tax consumption instead of the return from savings/investments in order to provide an incentive (or at least neutralise the disincentive) towards the latter.

Fourth, step (D) concerns the phenomenon of saving in perpetuity (i.e. to provide a legacy). We will deal with steps (A) through (C) first while elaborating on step (D) afterwards.

When it comes to step (A) – the incentive to produce – it is clear that the only thing that is happening is that the point at which the tax falls due is simply being shifted. The implicit “production good/consumption bad” mentality forgets the fact that production and consumption are opposite sides of the same coin – the purpose of all production is to consume. The value of all production is therefore derived from its ability to increase consumption. The greater the produced product that one can obtain from an act of production then the greater is one’s ability to consume; thus, the more productive an act of production then the more highly it will be valued. If a tax is levied at the point of production then one’s ability to consume is reduced and so the value of producing will diminish concomitantly. There will, therefore, be less production. But if a tax is levied at the point of consumption then the state is still taking some of the produced product away and one’s ability to consume is still diminished; hence, the value of producing is still reduced. Consequently there is unlikely to be any meaningful increase in the incentive to work and people will end up with the same de facto income regardless of when the tax is levied.

Regarding step (B) – the fact that, under an income tax, one’s income is taxed regardless of whether it is either consumed or saved – if people save in order to consume in the future then it is obvious that they do not avoid any consumption tax at all; they merely delay it. Once an investment is disinvested and consumed then these expenditures will be subject to the tax.

However, the “clever” argument here is that a tax on consumption taking effect in the future will be discounted by time preference and so will be perceived, by the individual, as a lower cost than a tax that is paid on income upfront. Or, to put it another way, if people have to pay their income tax upfront then that money is lost to them forever. If, on the other hand, they can hold onto it they can, in the meantime, save and invest it to earn a return. Thus, so the argument goes, people will be incentivised to save more as they seek to shift a portion of their tax burden to the future.

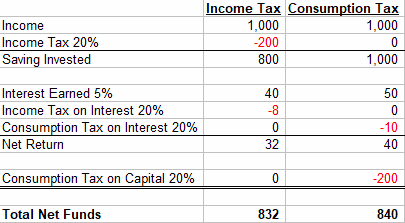

To illustrate, if a person has an income of £1,000 which is subject to a 20% income tax, he will pay a tax of £200 upfront. If he saves the remaining £800 at an interest rate of 5% he will earn, after one year, a return of £40, upon which he will pay an income tax of £8. His net return will be £32. If, on the other hand, the same income is subjected to a consumption tax of 20% he can save the full £1,000 and, at an interest rate of 5%, earn a return of £50 after one year, upon the disinvestment of which he will pay the £200 tax on the original £1,000 of capital and £10 tax on the return of £50, giving him a now higher net return of £40. Thus, so the argument goes, the possibility of increased net returns makes saving more attractive.6 In tabular form:

Unfortunately, there at least three problems with this as an argument in favour of a consumption tax.

First, the outcome of this in practice is that people will be paying an effectively lower tax rate today. This is because they pay tax only on the portion of their income that they consume which, as a percentage of their total income, must be lower than the headline tax rate.

For instance, let’s say that a person earns £100,000 and his desired consumption/saving preference is 80:20 of his net income. If the state imposes an income tax of 20%, he will pay a tax of £20,000, and of the remaining £80,000, he will consume £64,000 and save £16,000.

If, on the other hand, the state switches to a consumption tax of 20%, the individual will arrange his affairs so that he consumes £69,000, pays a tax on this consumption of £14,000 (i.e. 20% of £69,000), and saves an increased amount of £17,000 (i.e. 20% of his net income of £86,000). However, the tax of £14,000 expressed as a percentage of his gross income of £100,000 is only 14%, not 20%. Again, in tabular form:

Unfortunately for our consumption tax this fact raises the following question: could we not achieve the same result of increased saving simply by slashing the income tax rate to 14%? Why bother with the scenic route of rewriting the entire tax code and changing the entire tax bureaucracy if we can just change a number instead?7 Indeed, the entire argument concedes the point that the rate of saving has been increased because the amount of money flowing into state coffers today is lower.

Second, because of this realisation we can see that the benefits of a consumption tax will only materialise if the state can stomach the immediate drop to its revenue. In other words, the tax cannot be introduced successfully in the absence of an understanding of the benefits of lowering taxes. Most likely the state will simply impose the consumption tax at a higher rate which will offset any advantage to savings. Hence, if one is likely to have to argue for lower tax rates anyway why not just do so in regards to the existing income tax rate? Moreover, even if the consumption tax was imposed at the same rate as the existing income tax, the effect of the discounting in favour of saving would need to be underpinned by the certainty of a relatively stable tax regime that presents little or no possibility of the rate being raised in the future. The reader will have to judge for himself how likely this is to be. At least with an income tax the whole thing is done and dusted now, and any further predation on the same income will have to take effect as a new wealth tax (something which, both politically and administratively, is harder to do than simply increasing the rates of existing taxes). In fact, the only conclusive way in which one could incentivise saving ahead of consumption is if the consumption tax was expected to be dramatically lowered or even abolished at some point in the future.

Third, and to reiterate more or less the same points, if one really wants to invoke the role of time preference in the incentive to save/invest then surely one should acknowledge that the more critical factor is whether a person has more disposable funds in the first place? Is it not the case that satisfying more of people’s present, marginal wants is the element that will conclusively serve to lower time preferences and, thus, induce more saving? And is not the only way to do this through the tax system to cut taxes?

Step (C) concerns an income tax on the return from savings and investments. The argument here is that such a tax on the returns on savings/investment penalises future consumption but not present consumption; all else being equal, therefore, there will be more present consumption and less saving and investment as a result of the tax on the latter. Consequently, one should tax consumption rather than the returns on saving or investment.8

Unfortunately, however, the problem is exactly the same as that regarding the taxation of the capital. These returns will also be subject to the consumption tax once they are withdrawn and spent in the future. So, once again, if someone is saving to consume in the future he does not avoid the tax – he simply delays the point at which he has to pay it. Thus all of the counterarguments that apply to taxing the capital only upon its consumption apply also to taxing the returns from investing that capital.

Step (D) concerns saving in perpetuity – where one saves not to consume at some point in the future but to provide a stock of capital that will exceed one’s own lifespan. This phenomenon is the reason why people have inheritances to bequeath – they have not consumed all of their accumulated capital at the point they die. Rather, they have retained something, and often something very significant, that they can pass on to the next generation. So too will the inheriting generation then pass this wealth onto their children when the time comes; then it will be passed on to the fourth generation, and so on, the pie getting larger and larger as each generation contributes to it. Indeed, the snowballing bequests of our ancestors are the reason why, hitherto, the standard of living of each generation has exceeded that of previous generations. If this had not occurred and everybody had, instead, consumed all of their savings before they died then every generation would have found itself back at square one – having to build up from nothing instead of being able to stand on the shoulders of their forefathers. Consequently, from the point of view of economic progress, this is the most important type of saving there is.

Ignoring the possibility of death duties (which are a variety of a wealth tax and, thus, the biggest burden on saving in perpetuity), if the state chooses to tax dividends and capital gains regardless of the purpose of saving then the returns on saving in perpetuity and on saving to consume in the future are taxed in exactly the same way. Thus, according to step (C), a tax on consumption would ensure that more savings remain invested forever, leading to ever greater heights of prosperity.

Surely here we have an ingenious argument in favour of our consumption tax? For won’t the effect of the tax be to dissuade people permanently from consuming and, thus, they will save and invest so as to avoid the consumption tax forever?

Unfortunately, this is not the case. In the first place, the effect of a consumption tax that takes effect on disinvestment of assets is to render one avenue for the future use of assets (consumption) more costly and, thus, those assets are less useful than they otherwise would be if the tax did not exist. Consequently, the height of the tax levy to be applied upon a disinvestment will be discounted and capitalised in the value of the assets. In other words, the mere existence of the tax causes asset values as a whole to diminish, even if there is no disinvestment which is ever actually charged.

The bigger problem, however, is that the basic premise behind taxing consumption rather than savings/investments is flawed – a tax on consumption, like any other tax, will wind up being a tax on savings and investments anyway.

The reason for this is that the return on savings/investments depends upon the profit margins generated by selling the products that are produced with the invested assets. If the state taxes the consumption of these products then profit margins will be lower and so all that will result is lower gross returns from saving in the first place. These lower gross returns will, in turn, serve to depress the value of investment assets. Or, to put it in a more “Austrian” way even if you refrain from consuming yourself, the value of your investments is derived from their ability to increase the consumption of other people. If an additional cost is heaped upon these consumers then this cost will be imputed back to the value of the factors of production, i.e. the assets that comprise one’s investments. Thus, it is saving and investment that is ultimately penalised by the consumption tax.

Indeed, the basic economic theorem – that if you increase taxes on activity A while reducing taxes on activity B so that the incidence of activity A will decrease while the incidence of activity B will increase – is true only if activities A and B are unrelated. For instance, if the government wishes to discourage the purchase of alcohol while encouraging the purchase of fluffy bunny toys (perhaps to put into “safe spaces”), a sufficient increase in taxes on alcohol and a concomitant decrease in taxes on fluffy bunnies will ensure that the desired effect is achieved. There will be fewer purchases of alcoholic beverages and more purchases of fluffy bunnies, with productive assets flowing out of the breweries and into the soft toy factories.

When it comes to consumption vs. saving/investment, a consumption tax could only work to stimulate the latter if it served to raise the cost of consuming in relation to the cost of saving (or, to put it another way, if the benefit of saving rose in relation to the benefit of consuming). This is what the most naïve proponents of the consumption tax would like you to believe. Indeed, always lurking in the background of proposals for a consumption tax is the faux moral argument that consumption, like drinking alcohol, is a vice for which people should be penalised whereas saving and production are beneficial acts which should either be left undisturbed or encouraged.9 However, such notions are clearly ridiculous; because the value of all saving is, ultimately, derived from its ability to increase consumption, a consumption tax must lower the benefit of saving also.

Indeed, all of these things – production, earning, saving, investment, etc. – are simply events, or way stations, that occur on what is basically the same journey to the destination of consumption. Ransacking the train at any point – before or after it reaches that destination – will depress the motivation to begin the whole journey. In other words, the overall effect of taxing a person’s consumption will be to penalise his entire productive lifestyle – i.e. both his consumption and his saving – in favour of non-monetary acts of consumption (such as increased leisure time).

Finally, and for the sake of completion, because the effect of any tax is to confiscate money from the productive citizenry and to spend it on what the state wants instead of what they (the citizens) want, revenues and profits will flow out of industries servicing the needs of ordinary people and into industries servicing the needs of the state. Consequently, investment will shift also from industries serving consumers into industries that feed government consumption. Instead of more investment in cheaper food, clothing, cars and so on more money will be put into bureaucracies and boondoggles. Thus, the ultimate effect of any tax – including a tax on consumption – is to penalise saving and investment in productive enterprises to the benefit of “investment” in non-productive enterprises that service government waste. The result, of course, is diminished economic prosperity.

Therefore, taking the proposal for a consumption tax in its entirety, step (A) will not cause anyone to work any harder to produce in the first place; once they have produced, steps (B) and (C) will not cause them to have any greater incentive towards saving/investment ahead of consumption (or at least not in any way that is advantageous to simply cutting income taxes); and, once they have invested, step (D) will not cause them to have any greater incentive towards saving in perpetuity ahead of disinvesting and consuming what they have saved. All options are penalised to the extent that it cannot be stated conclusively that a preference is likely to be made either way.

So whichever way you look at it a tax on consumption, by merely shifting a tax liability around, does nothing to eliminate, convincingly, the negative effects of tax on production – there is no free lunch.

Foreign Investment and Government Incentives under a Consumption Tax

Ironically, the one convincing economic benefit that a consumption tax would bring may wind up causing its demise anyway. This benefit is owing to the fact that the consumption tax would replace any taxes on the profits earned by businesses, those profits being taxed only when they are distributed and consumed by investors. In short, companies would pay no tax. Such an abolition of corporate taxes would cause an influx of investment capital from abroad as foreign investors and companies set up UK subsidiaries to take advantage of what would effectively become the world’s biggest tax haven, boosting UK industry and creating a concomitant demand for jobs and higher wages. In fact, even if most of this cash was not invested directly in UK industry, this sceptred isle would become the preferred conduit for tax free capital flows, requiring specialist financial services, accountants and overseers to manage this huge pile of wealth. All well and good, one might say.

Unfortunately, this would not amount to much of an argument in favour of a consumption tax and, in fact, reveals some of the flaws that are unique to this mode of taxation.

In the first place, the UK would experience these benefits only to the extent that foreign countries retained their existing corporation tax structures and refrained from switching to a consumption tax themselves. Presumably it is not the intention of the proponents of a consumption tax that it be applied in only a handful of countries and that they would prefer for their vision to be realised across the entire world? If so, as soon as other countries adopt the plan then any competitive tax advantage for the UK would be lost.

Second, and once again, all that we have ended up demonstrating is that what really stimulates investment is lower tax rates. Indeed, the same effects could be achieved by just lowering the corporation tax rate to below the rate of the same in other countries. Why not just take this simple and straightforward route instead of fussing around with a consumption tax?

The final problem concerns the fact that, when we are talking about foreign investment, switching from taxing income to taxing consumption brings with it a change in the jurisdiction of the taxable event. Thus, regardless of whether a consumption tax brings about any change to the total amount of tax that is paid, it will bring about a change of government to whom that tax flows.

Although different states have different rules, an income tax normally falls due in the jurisdiction from which the income is sourced and/or where the taxed individual or entity is resident. So, for example, regardless of the nationality of its investors, a company based in the UK and making its profits from operations in the UK will pay tax to the UK government; a company doing the same in France will pay tax to the French government, and so on.

A consumption tax, however, is applied in the jurisdiction not where the income is sourced but where it is spent. Thus, under a consumption tax, while we would see a vast quantity of new wealth from foreign investment being earned in the UK practically none of it would be consumed in the UK for the simple reason that the investors who own it reside abroad – they will transfer it to their home countries before consuming it there. Therefore, none of this money would, at any point, bring in any revenue for the UK government.

This fact is a boon for the libertarian, of course – but what are the chances that the government will simply sit back and watch all of these profits and dividends flow out of the country into foreign bank accounts without so much as a gratuity to the government that has provided the stability and security of this wonderful, business friendly jurisdiction? How likely is it that the state will allow outfits such as Amazon or Google to benefit from publicly funded infrastructure without having to pay a penny for it? Indeed, the amount of tax (not) paid by such foreign entities is already controversial. How much more likely is it to be so under a consumption tax where they would effectively pay nothing?

To ask these questions is to answer them. The likely result is that a special tax would be introduced on the transfer of profits abroad – or, more simply, such a transfer would be defined, for tax purposes, as consumption, and thus subjected to the consumption tax. Therefore, one way or another, the result would be the reinstatement of a de facto income tax and any gains from foreign investment would be obliterated.

Indeed, if consumption taxes replaced income taxes worldwide then the natural result would be massive a transfer of the ownership of wealth from countries in which it is cheapest to produce to countries in which it is cheapest to consume. The governments of countries which possess investment potential for reasons other than tax – such as an abundance of natural resources – are not likely to sit idly by and watch all of the wealth generated from their land be plundered by foreigners with all the tax benefits flowing into the coffers of alien governments who have done nothing to help create it.

If, however, governments did somehow manage to restrict themselves to taxing only consumption within their shores then the natural result of making all state revenue dependent upon consumption is that states would have no interest in promoting production and every interest in promoting consumption. In other words, all of the planning and regulatory environment will be skewered to make everything as easy as possible for consumer facing industries in order to maximise consumer spending and, in turn, inflate government revenue, while in turn making it as difficult as possible for industries that invest in the production of higher order capital goods. Instead of investment in factories and raw materials every country would be racing to turn itself into a giant shopping mall. States would shun the prospect of attracting rich investors and entrepreneurs in favour of bringing in big spenders and wasters – an endeavour to which the needs of businesses and production might even become something of a nuisance. Every state would, of course, have a motivation to lower its consumption taxes so that wealthy foreigners are more likely to move there and spend their cash. But, once again, this just raises the same question we have been asking all along: why not just cut income taxes and achieve the same outcome while avoiding all of these vicissitudes by keeping the government focussed on the need for continued production rather than continued consumption? Indeed, false theories of “under-consumptionism” already plague government economic policy to the detriment of prosperity. Why are proponents of the consumption tax so keen to make this worse? Given the state’s voracious appetite for spending, the likely outcome is that shortfalls in revenue will eventually lead to increased wealth taxes, or, at least, taxes on saved or hoarded cash, precisely to encourage people to spend – something which negative interest rate policy has already tried to achieve. At the very least we could expect spending to be morphed into a patriotic duty in order to prop up “our” NHS.

Libertarian Considerations

The consumption tax also has a number of distinct disadvantages from a purely libertarian perspective. In fact, the worst case scenario is that it could end up sounding the death knell for whatever vestige of financial privacy remains.

If it is applied regressively, i.e. as some form of VAT or sales tax lumped onto the sale of every item, then, unless the rates were exceptionally low, the concomitant price rises in basic and “essential” consumer goods would spur the creation of a black market in practically everything. We are used to hearing of contraband cigarettes and brandy, but a consumption tax could make contraband bread, milk and Weetabix a reality as the lowest earners in society (who spend the majority of their income on basic consumption items such as food) are incentivised to take on the role of society’s biggest tax avoiders. Consequently, enforcement of the consumption tax would simply add another weapon in the arsenal of the state’s war on cash as the state seeks to ban untraceable and unrecorded transactions.

The more likely scenario, however, would be for the consumption tax to be applied progressively so that the wealthier are burdened more than the poor (as the ASI proposes). As businesses do not know whether they are selling to a higher rate tax payer or to a lower rate tax payer (and, in any case, the idea of having “different” price labels for different people is woefully impractical) the tax could not be applied at the point of sale and so the black market problem would be avoided. But the most likely, practical manner of taxing consumption progressively while, at the same time, ensuring compliance is for the withholding tax on income to remain in place, with people then claiming a refund, in various tax brackets, for all net contributions made to savings and investments during the past tax year.10 This would have the effect of expanding the state’s tentacles into all varieties of saving and investment, both private and public, whether these are in stocks, bonds, bank accounts, property, privately owned enterprises, or whatever – with only investments in “approved” channels monitored by the state being eligible for a tax refund. Withdrawing one’s cash from the bank to put into a safe or to buy gold coins from a private dealer would, no doubt, fail to qualify.

Consequently, a progressive consumption tax could end up being a backdoor method of imposing capital controls, with the state using it as a mechanism to keep as much cash as possible locked up in its dangerously insolvent financial system. Indeed, with most governments nearing bankruptcy from their inability to fund generous benefits and entitlements, it would not be surprising if, one day, we could end up seeing every transaction classified as taxable “consumption” except for purchases of government bonds and deposits in domestic banks. There is, after all, no guarantee that the state will take a reasonable view of which transactions will be defined as “consumption” for tax purposes.

A final possible issue to which only libertarians may be sympathetic concerns, again, taxes on companies and business entities. As we noted earlier, the consumption tax would replace any taxes on profits earned by such entities and on dividends they distribute to investors. A tax would, on the other hand, be paid once these profits are disinvested and consumed by the investors.

At the moment, businesses can employ an army of accountants and tax specialists who are able to exploit accounting rules and loopholes in order to manipulate the size of the chargeable profit and thus pay a lower amount of tax. In other words, legal corporate tax avoidance remains eminently possible when the tax payable is assessed according to income. Thus, more capital remains within companies to deploy as they see fit and outside of the hands of the state.

If, however, payment of the tax is switched from the point at which the company earns the profit to the point at which the investors spend those profits once distributed then all of this opportunity would be lost. If a consumption tax is regressive, of course, then the investor would have no choice whatsoever – he simply has to pay the price of goods that he wants with a fixed portion of that price being paid to the state. If, on the other hand, the tax is applied progressively and requires the filing of a return then investors may, of course, seek the services of tax advisors who will attempt to reduce as much of their income as possible that can be classified as “consumption”. While no one should underestimate the creative genius of tax accountants, is it not likely there will be fewer grey areas in the difference between the legal definition of “consuming” and “saving” than there is when wrestling with the myriad of charges on a company’s income statement? If so then it could be argued that, in this respect, a direct tax on saving and investment is preferable to a consumption tax.

The only mercy in all of this may come from the logistical nightmare that the state may inflict upon itself as a result of implementing a progressive consumption tax.

The first of these is what to do with regards to existing savings and investments at the point the consumption tax is introduced. Much of this wealth has already been taxed under prior income tax rules, and so if the consumption tax was to be imposed upon the disinvestment of these assets they would, in effect, be taxed twice – a hefty to blow to someone who has saved up a nest egg for years and years outside of a tax-free vehicle. The only way to avoid an unfair penalty to the holders of existing wealth would be the bureaucratic headache of a mass closure of existing investment funds and savings accounts to new contributions in order to segregate “old” money from “new”. This may also require the administration of old tax rules on say, capital gains and dividends, to continue for those old investments for decades to come – thus making taxation more ludicrously complicated rather than more straightforward.

Second is the fact that tens of millions of relatively low or moderate income earning citizens may suddenly find themselves having to complete a tax return in order to claim refunds on the portion of their income they have saved or invested (although, to be fair, if a person’s saving/investment choices were relatively simple – say into bank savings accounts or pensions and mutual funds from domestic providers – the refund could be made automatically by these institutions to “top up” the amount saved directly). If so, the revenue bureaucracy would be swamped by tens of millions of tax returns come January 31st. One or two incidences of a significant number of people failing to receive their refunds on time and correctly, coupled with tabloid headlines of “huge” refunds being paid to “the rich” on account of their high levels of saving may well be enough for the whole scheme to be scrapped.

Conclusion

In spite of the specific problems that are unique to the consumption tax, it is worth reiterating the point that the greatest economic burden exerted by taxation stems from the height at which those taxes are imposed rather than from their form.11 Thus, the majority of what has been said here should not be taken to mean that consumption taxes are necessarily worse compared to any other kind of tax, at least not to a tremendous degree. Indeed, if we had them already instead of income taxes one might well be largely indifferent to the fact.

Rather, the particular point that needs to be emphasised is that the proposal to switch from the present array of taxes to a consumption tax is largely irrelevant for a programme that is serious about making inroads to relieving the burden of tax on economic prosperity. Such a switch promises nuanced benefits that lack both the solid conviction and simplicity of simply cutting the existing taxes on income, in return for the gargantuan effort and expense of rewriting the tax code and reorienting individuals, business, accountants and bureaucrats towards an entirely new compliance environment – a environment that makes no solid promises in terms of reducing tax bureaucracy and every promise of continuing and augmenting the state’s depredations upon financial privacy.

This does not mean to say that reforming the tax code one way or another should not be an eventual aim. However, at the stage we are at currently it is very unlikely that such a reformation can make any significant inroad into lowering the economic burden of taxation without also convincing both the public and the taxing authorities that taxes must, one way or another, be lower. As we indicated in the previous essay:

The type of gradation itself says nothing about the rates of tax that are imposed […] A progressive system with a top rate of 20% will be better than a flat tax at a rate of 30%, whereas, conversely, a flat tax at a rate of 20% would be better than a progressive tax with a starting rate of 30%. The outcome of a lower tax burden is therefore not guaranteed solely by the type of tax system.12

Similarly there would be little point in switching to a consumption tax if the state obliterated whatever savings were achieved by jacking up the rate to an absurd level.

Radical and pioneering tax reform programmes need to start, therefore, with the simplest and most effective task: lowering the rates on existing taxes and orienting both the people and the government to the benefits of lower taxes. Only after that has been achieved may considering changes to the tax code for further gains be worthwhile. Indeed, given that such changes will always create perceived “winners” and “losers” from concomitant shifts in the tax burden, it may not even be possible to achieve such changes (nor overcome the use of tax for other purposes such as wealth redistribution and “social justice”) in the absence of a wider appreciation for lower taxes.

Thus, if we wish to take a sledge hammer to the burden of tax on prosperity, focussing on an endeavour such as the consumption tax, at least at this stage, is likely to be a waste of effort and resources – resources that free market institutions often have very few of. The fact of tax is the problem; moving it around does not fix that problem.

Notes

1Duncan Whitmore, Tackling Taxes for Economic Prosperity, https://misesuk.org/2018/07/30/tackling-taxes-for-economic-prosperity/.

2https://www.adamsmith.org/policy.

3Ibid.

4It is not the case that all such arguments repeat all of these steps verbatim, nor do they all necessarily strive towards the same objective – different arguments will usually emphasise some aspects and effects over others. What is being laid out here is as complete an exposition of the whole argument as is possible from the point of view of attempting to boost economic progress.

5A more sophisticated form of this argument is that an income tax represents some kind of increased or “double” taxation on savings and investments. The purported reason for this is if a person consumes £1,000 of his income then a £100 tax on this income will cost him only £100 in goods and services. If, however, he decides to save £1,000 the tax of £100 on that income will cost him more than £100 because that £100 would have provided a return. So if, say, the rate of interest is 5% and his period of saving is one year, he has, in fact, lost £105 rather than just £100 as a result of the tax. Thus, an income tax penalises the portion of one’s income that is saved more heavily than the portion that is consumed.

The argument is fallacious because it overlooks the fact that the loss of a return is a future loss which must be discounted to its present value – which, for £105 in a year’s time at an interest rate of 5% is, of course, £100. It is true that an income tax will serve to depress saving but the reason for this is that the loss of monetary assets serves to raise time preferences – a phenomenon that is shared by all taxes. Taking a person’s saving/consumption preference as a given, however, there is no reason why the effect of an income tax weighs especially heavily on the portion of his income that is saved rather than on the portion that is consumed.

6Needless to say the assumption that the interest rate would be equal under the two scenarios is entirely dubious. The whole effect of creating a preference for the future over the present is to lower the premium on present goods vis-à-vis future goods – in other words, to lower the interest rate. But we will ignore this factor for the sake of conceding to the consumption tax its best possible case.

7Cf. Murray N Rothbard, Man, Economy and State with Power and Market, Scholars’ Edition (2009), pp 1180-83.

8It is, however, doubtful whether the tax burden is weighted disproportionately on savings/investments in the UK in the manner described. The state already levies consumption taxes on a vast number of goods and services as well as taxing the return on savings/investments. The most that can be said is that consumption is taxed at a lower rate than saving and investment, but this may be true only for higher rate tax payers.

9As Murray N Rothbard puts it:

[There is] a curious tendency among economists generally devoted to the free market to be unwilling to consider its ratio of consumption to investment allocations as optimal. The economic case for the free market is that market allocations tend at all points to be optimal with respect to consumer desires. The economists who favor the free market recognize this in most areas of the economy but for some reason show a predilection for and special tenderness toward savings-investment, as against consumption. They tend to feel that a tax on saving is far more of an invasion of the free market than a tax on consumption. It is true that saving embodies future consumption. But people voluntarily choose between present and future consumption in accordance with their time preferences, and this voluntary choice is their optimal choice. Any tax levied particularly on their consumption, therefore, is just as much a distortion and invasion of the free market as a tax on their savings.

Rothbard, p.1170 (emphasis in the original).

10In fact, it is most likely that the existing VAT system would be retained (with, perhaps, some modification), while all income taxes are switched to progressive consumption taxes – thus we would end up with a mixture of progressive and regressive consumption taxes. This, indeed, is the ASI’s full proposal. This should provide food for thought for those who believe that a switch to a consumption tax would reduce the amount of bureaucracy required to administer tax affairs. Pretty much all of the existing infrastructure to enforce the withholding tax and the burden of VAT administration for businesses would remain in place, with the addition of increased monitoring and oversight of saving and investment vehicles. The only perceivable cut would come from the end to corporation taxes.

11With the major exception of taxes on wealth as opposed to taxes on incomes.

12Footnote 1.

Discover more from The Libertarian Alliance

Subscribe to get the latest posts sent to your email.