“Austrian” Business Cycle Theory – an “Easy” Explanation

By Duncan Whitmore

Compared to the simple and straightforward siren songs of “underconsumptionist” and “underspending” theories of boom and bust, “Austrian” business cycle theory (ABCT) can seem unduly complex. The former types of theory, associated with “mainstream” schools of economics, at least have the advantage of the veneer of plausibility, in spite of their falsehood. A glut of business confidence and spending will, it seems, naturally lead to an economic boom, a boom that can only come crashing down if these aspects were to disappear. For what could be worse for economic progress if people just don’t have the nerve do anything? Add in all of the usual traits of “greed” and “selfishness” with which people take pride in ascribing to bankers and businessmen (again, with demonstrable plausibility) and you have a pretty convincing cover story for why we routinely suffer from the business cycle. ABCT, on the other hand, with its long chains of deductive logic, can seem more impenetrable and confusing. Is there a way in which Austro-libertarians can overcome this problem?

“Austrian” economics is unique in that all its laws are deduced from a handful of self-evident truths (the most important being the action axiom), peppered with a few additional assumptions or empirical truths (such as the desire for more leisure time). The entire corpus of economic law – right from the isolated individual choosing between simple ends all the way up to complex structures of production, trade and finance – forms a unified and logically consistent whole.

This is not true, however, of “mainstream” schools of thought which tend, nowadays, to be splintered and scattered into separate, specialised areas of study that are based upon their own, individual foundations. The fissure between so-called “microeconomics” on the one hand and “macroeconomics” on the other is a case in point. Although it still contains many faults and general misunderstandings resulting from a lack of the coherence that would be furnished by deduction from the action axiom, “Austrians” will read much that is agreeable in “microeconomics”. “Macroeconomics”, however, seems to be a completely different ball game, considering only “the economy as a whole” without reference to its individual components1. It is this fact that “Austrians” can use to give them the upper hand when explaining the business cycle. For in ABCT, the explanations of “macro” phenomena are little more than an extension of what is found in “micro” price theory.

The equilibrium price for a good is the price at which the quantity demanded equals the quantity supplied. As a result of the competition of buyers and sellers the market price always tends towards the equilibrium price, and so such prices serve to ration goods as a response to their scarcity – the goods available are traded from the hands of the most eager sellers to those of the most eager buyers. Those buyers who are not willing to pay the market price will go away empty handed and those sellers who are unwilling to sell at the market price will not be able to get rid of their goods.

What happens, then, if this relationship is disturbed by a forced fixing of prices by the state?

First, if the price is raised above the market price to create a price floor, the new price will attract more sellers into the market for that good because the price that they will receive for a sale is now the (higher) price at which they are willing to sell. However, at this new price there are fewer people wishing to buy the good. Some buyers, who were not previously prepared to pay the lower, market price, are certainly not going to pay the higher price now, while those who would have paid the market price before may now decide that the new price is too high so they also do not buy. What results, therefore, is an increase in sellers and a decrease in buyers, which can lead to only one thing – a surplus of unsold inventory. The sellers may be very eager to sell at the new price but they will have a hard time finding anyone to whom they can sell.

Second, where the price is lowered below the market price (a price ceiling) the opposite effect is created. This new price will attract more buyers into the market for that good because the price that they will pay for a purchase is now the lower price at which they are willing to buy. However, at this lowered price there are fewer people wishing to sell the good. Again, some sellers, who were not, before, prepared to sell at the market price are certainly not going to sell at the lower price now, while those who would have sold at the market price may now decide that the new price is too low so they also do not sell2. What results, therefore, is a decrease in sellers and an increase in buyers which, clearly, leads only to a shortage of goods. Buyers will swarm into the marketplace eager to purchase the articles at the new, attractive price but, to their dismay, the shelves will be empty, cleared out by all of the hastier buyers who got there before them3.

It is this latter scenario – that of artificially lowered prices – that is relevant for ABCT. For the business cycle is, according to “Austrians”, little more than price fixing on the widest scale, the fixing and the manipulation of what is possibly the most important price in the economy – the interest rate on the loan market. Rather than being the price at which a single good is traded, the interest rate is the price at which saved funds are borrowed and lent (i.e. demanded and supplied) in the economy.4

When the stock of money is not subject to state interference, if one person wants to borrow (demand) money then another must have saved it in order to lend (supply) it. The resulting rate of interest is the point at which the quantity of money lent equals the quantity of money borrowed. Any borrowers who want to borrow at a cheaper rate and any sellers who want to lend at a higher rate will find themselves priced out of the market for loanable funds. This situation produces a stable amount of saving, lending, borrowing and investment because the interest rate – the price of saved funds – is in harmony with the preferences of consumers, in particular, their preferences for allocating their funds towards either capital or consumer goods. The portion of his funds that the saver retains for consumption will be spent on consumer goods (i.e., present consumption) whereas the portion that he allocates towards saving and lending for investment will be spent on capital goods that will not provide any immediate consumption but will provide a greater amount of it in the future.

At the market rate of interest goods and resources in the economy will be allocated in harmony with these desires. If, for example, a borrower wishes to borrow money to build a factory (a capital good) and his calculations reveal that the prevailing rate of interest is low enough for him to make a return on this enterprise, it means that savers are willing to lend a sufficient quantity of funds in order to make this project viable. If, however, the prevailing interest rate is too high it means that savers are not willing to lend enough funds to build the factory – the money that could be spent on building the factory they would prefer to spend on their own, immediate consumption. What happens, then, if the rate of interest is set below the equilibrium rate?5 Exactly the same as what happens when prices are forcibly lowered for any single good. At this rate borrowers who previously found the rate of interest too high for their ventures now find that they can afford to borrow. The quantity of funds demanded, therefore, will rise at this new, low price. Savers, however, will be less willing to lend at this price. Certainly if they weren’t prepared to lend at the previous rate of interest they will not be induced to do so by an even lower rate, and some savers who were prepared to lend at the market rate will not be prepared to do so at the new, artificially fixed rate. The increase in borrowers and decrease in sellers, therefore, causes a shortage of saved funds, or at least it should do so. Why, then, does this shortage not materialise immediately at the point that the interest rate is fixed? Why aren’t the banks cleared out of cash, and why can they keep on lending and lending? Why can this situation perpetuate for years and end in a calamitous crash that causes almost unrelenting havoc?

This is where a degree of complexity enters the explanation. In a loan contract, what is really being borrowed and lent is not money but, rather, the real goods and resources which that money can buy.6 If a construction firm borrows money to build a row of houses what it really wants is the bricks, cement, roofing tiles, etc. that will be bought with the borrowed money. We said above that if someone wishes to borrow money another person has to have saved it. What this really means is that the saver has to have worked to produce real goods and resources in order to earn that money. He then lends that money to the borrower and the borrower uses that money to buy those goods that the lender produced and diverts them towards his enterprise.

If, of course, saving, lending and borrowing took place with real goods, or if the supply of money was fixed, then obviously a forced lowering of the rate at which these goods could be borrowed would result in their shortage very quickly. But the fact that the saving and lending takes place through the mechanism of an easily expanded paper money supply creates a clever smokescreen. For our entire financial system rests not on the principle of every pound borrowed requiring a pound to be saved, but rather that pounds can be “created” out of thin air through the fractional reserve system before being lent out even though someone has not saved. By printing fresh money (or its digital equivalent) the volume of borrowing can expand without a corresponding expansion of the volume of saving. This easy ability to produce more money to meet the higher demand for borrowing means that the artificially low interest rate never causes a shortage of money as we would normally expect when the price of any other good is fixed below its market price.

A second problem, though, is that the real goods that this new money can buy have not increased in line with the increase of the supply of money, but, rather, have remained constant. There is, therefore, still the same quantity of goods that have to be allocated towards either consumption or investment. Surely the artificially low interest rate will mean that there will be a shortage of real goods to devote towards investment?

Unfortunately, at the beginning, this is not so. For the newly printed money transfers purchasing power over goods out of the hands of those holding existing money and into the hands of those who have the new money. The result of this is that the borrowers of the new money – those who want to devote the goods purchased to capital investment – now have an advantage over those who wish to devote them to consumption.

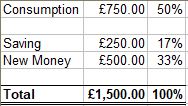

Let’s say, for example, that I earn £1,000 in a given month. This means that I have worked for and created real goods in the economy on which I can spend this £1,000. Let’s then say that I allocate £750 towards consumption and £250 towards saving and investment. Therefore, what I want to achieve is to consume 75% of the goods on which I can spend the money and save and invest 25%. This £250, the 25% of the goods I wish to devote to saving and lending, constitutes a supply in the loan market that will help to set the market rate of interest. We can illustrate this allocation accordingly:

If, however, a commercial bank depresses the interest rate and simply prints an extra £500 to meet the new demand for borrowing at this lower rate, what has happened now? There has been no change, remember, in the quantity of goods – the new money must be still be spent on these goods. The purchasing power of the existing money that I wished to spend on consumption therefore reduces and that of the new money that is to be spent on lending and investment correspondingly increases. All that happens therefore is that the proportion of goods that can be devoted to lending and, hence, to investment has now been forcibly increased from £250 to £750 – and increase from 25% to 50% of the new, total stock of money, thus:

Newly printed money that enters the loan market therefore forces the economy onto a different consumption/investment ratio from that which is desired by consumers. The poor consumer will find that the newly created money has caused the prices of his consumer goods to rise; he is forced, therefore, to curtail his consumption in real terms. The goods that he can no longer afford to buy and consume will be purchased by the new borrowers who will devote them towards their enterprises. It is for this reason that none of the expected effects of price fixing occur and the economy proceeds along what appears to be a sustainable boom in capital investment.

The problem, though, is that capital projects usually take several years to complete and rely on a continuous supply of goods throughout this time. But consumers don’t want to save voluntarily the amount necessary to complete these projects. The interest rate must therefore be kept at a constant, artificially low rate, and the new money must be kept reeling off the printers to sustain this rate if the projects are to continue. It is only down the line when price inflation inevitably begins to accelerate and the central bank forces an increase in the interest rate coupled with a corresponding reduction in growth of the money supply that the problems are revealed. For now the consumption/investment ratio once again begins to reflect the preferences of consumers – they want, if we remember, more consumption and less saving which means that lending and investment has to reduce. Hence, it is at this point that half-finished capital projects have to be left incomplete. They have been starved of the resources necessary to complete them as they can no longer afford to purchase these resources at the new (higher) rate of interest. This precipitates a collapse in the prices of capital assets, a collapse that causes widespread bankruptcy and liquidation of firms and enterprises that, hitherto, had seemed sustainable and profitable.

Ludwig von Mises describes the perfect analogy:

The whole entrepreneurial class is, as it were, in the position of a master-builder whose task it is to erect a building out of a limited supply of building materials. If this man overestimates the quantity of the available supply, he drafts a plan for the execution of which the means at his disposal are not sufficient. He oversizes the groundwork and the foundations and only discovers later in the progress of the construction that he lacks the material needed for the completion of the structure. It is obvious that our master-builder’s fault was not overinvestment, but an inappropriate employment of the means at his disposal7.

Mises’ last sentence is important. As the prices of capital goods were accelerating upwards during the boom before crashing suddenly, there is a temptation to analyse the situation as one of “overinvestment”. While this is true and that “too much” has been devoted to long term investment projects it should be clear from our analysis that the real problem is malinvestment – a diversion of resources from desired consumer goods to capital goods.

Observant readers may suggest that it is actually the return to the market rate of interest rather than the fixed rate that has caused the sudden shortage of capital goods. This would not be a correct interpretation. Artificially lower prices always give the illusion of plenty – of abundance and availability for everyone. It is just that with the fixed price of a particular good the illusion becomes obvious more quickly. But with fixing the rate of interest, because it takes effect through the mechanism of money, the illusion of plenty is obscured and, for a time, looks very sound. For this new money has the very real ability to divert resources away from consumption towards capital investment. Nothing more has been created but it looks like there has. Couple that with price inflation and with higher nominal wages then people think that they are better off than they were before the “miracle” of artificially low interest rates. Real abundance and plenty, however, would not merely divert resources from the desired level of consumption. Rather, resources for capital investment would exist independently of and in addition to those desired for consumption, as dictated by the desires of consumers.

Conclusion

What we have seen, therefore, is that ABCT sits coherently with the examination of individual price action and is little more than an extension of it. The business cycle is simply a case of price fixing writ large, causing widespread waste, chaos and misery when its effects are finally revealed. There are no separate bases or foundations of this “macro” sphere of economic theory. There are, however, certain special features that make this form of price fixing especially insidious and long-lasting – that of the easy ability to print fresh money to meet the new, low rate of interest, permitting purchasing power to be transferred to new borrowers and, hence, the real diversion of resources. As soon as this situation ceases the smokescreens vanish to reveal the waste and futility of these diversions.

Whenever, therefore, one has difficulty in either understanding or explaining ABCT, think back to what you know about simple price fixing. In fixing the rate of interest, the most important price in the economy, “Austrian” economics will tell you that the results will be the same.

Notes

1Murray N Rothbard, Man Economy, and State with Power and Market, Scholars’ Edition, Ludwig von Mises Institute (2009), p. 269 (n. 19).

2This isn’t just stinginess on the part of sellers; rather, the cause of their unwillingness to sell will be, in the long run, that they simply cannot – the lower price will usually not be sufficient for them to recoup the costs of production so they have to abandon the particular line altogether.

3These results were seen during the high inflation of the 1970s in the US when price controls led to long queues at gasoline station because the demanded quantity of gasoline could not be supplied at the artificially low price. They have also been seen more recently as a result of price controls in Venezuela.

4An interesting question is whether the interest rate may be considered as a “price” like any other. In the exchange of goods, the price of a good is the quantity of another good that is fetched in exchange between the two. For example, if one apple sells for two oranges, then the “orange” price of an apple is two oranges (and the “apple” price of an orange is 0.5 apples). In the complex economy, of course, every good is exchanged for money so we always reckon prices in terms of the quantity of money received in exchange. However, whichever other good that is received, it makes no sense to compare two physically heterogeneous goods in terms of magnitude. For how does one calculate the “difference” between two apples and one orange, or between £2 and a bag of oranges? In the exchange of a present good for a future good, which is what happens in the loan market, this is not the case, however. If a borrower agrees with a lender to borrow £100 today and to pay back £110 in one year’s time, strictly speaking the price of one unit of present money is 1.1 units of future money (or the price of 1 unit of future money is approximately 0.91 units of present money). But because the two goods are physically homogenous we can compare the two magnitudes – 1.0 and 1.1 – in order to derive a rate or ratio between them of 10%. We would therefore state that the interest rate per annum in this scenario is 10%. This rate is therefore not strictly a price but an expression of two prices – the price of present money in terms of future money and the price of future money in terms of present money. However, it should be clear that a manipulation of the rate of interest would have the effect of fixing the actual prices of present and future money. If, for example, the interest rate is forcibly lowered to 5% then the price of one unit of present money is now 1.05 units of future money rather than 1.1 units of future money. The resulting effects of price fixing will therefore be felt in this scenario. Hence, it makes sense to speak of the rate of interest as a price just like any other and, indeed, this is how it is treated by acting humans in the loan market (as the payment of interest is a real cost that must be borne).

5On a technical note, we should mention the fact that there is no such thing as the rate of interest in the marketplace. A buyer can expect to pay the same price as everyone else when the goods he purchases are homogenous (so everyone who buys the same brand of apples in the same supermarket at the same time will pay neither more nor less than anyone else). Loans that are advanced on the loan market do not, however, enjoy such homogeneity for the reason that interest rates that are actually charged reflect, in addition to time preference, the risk of the specific enterprise failing as well as premiums for expected inflation. Indeed, it may be the case that post-credit expansion loans are advanced with interest rates that are higher than those on loans advanced prior to the credit expansion. Rather than saying that credit expansion reduces “the” rate of interest it is more accurate to say that loans are advanced on rates that would not be agreed in the absence of the expansion of credit.

6Cf. Ludwig von Mises, The Theory of Money and Credit, Ludwig von Mises Institute (2009), p. 340.

7Ludwig von Mises, Human Action: A Treatise on Economics, The Scholars’ Edition, Ludwig von Mises Institute (1998), p. 557.

Discover more from The Libertarian Alliance

Subscribe to get the latest posts sent to your email.